Understanding net profit margin is crucial for any business, regardless of size or industry. It’s a key indicator of profitability, revealing how efficiently a company converts revenue into actual profit. This guide delves into the intricacies of net profit margin, exploring its calculation, analysis, and strategic implications for business growth and decision-making.

We’ll examine how various factors, both internal (like cost management and pricing strategies) and external (such as market conditions and competition), influence net profit margin. We will also compare and contrast net profit margin with other profitability metrics, providing a holistic perspective on financial health. By the end, you’ll possess a robust understanding of this vital financial metric and its practical applications.

Net Profit Margin and Profitability

Net profit margin is a crucial financial metric that directly reflects a company’s overall profitability. It represents the percentage of revenue remaining after all expenses, including taxes and interest, have been deducted. A higher net profit margin indicates greater efficiency and stronger financial health, while a lower margin suggests areas needing improvement in cost management or revenue generation.Net profit margin and overall profitability are intrinsically linked.

The net profit margin is, in essence, a concise summary of a company’s profitability. A high net profit margin demonstrates that a company is effectively converting its revenue into profit, indicating strong operational efficiency and potentially a competitive advantage in the marketplace. Conversely, a low net profit margin may signal inefficiencies, high operating costs, or intense competition pressuring prices.

Analyzing this metric alongside other profitability ratios provides a comprehensive view of a company’s financial performance.

Strategic Decision-Making Using Net Profit Margin

Businesses utilize net profit margin data for various strategic decisions. For instance, a company consistently showing a declining net profit margin might investigate cost-cutting measures, explore new revenue streams, or reassess its pricing strategy. Imagine a retail company experiencing shrinking margins. Analyzing the data, they might discover that rising operational costs due to inefficient inventory management are the primary culprit.

This insight allows them to implement strategies like improved inventory tracking systems or renegotiating supplier contracts to restore profitability. Alternatively, a company with a consistently high net profit margin might consider expanding its operations, investing in research and development, or acquiring competitors, confident in its ability to generate substantial returns.

Best Practices for Maintaining a Healthy Net Profit Margin

Maintaining a healthy net profit margin requires a multifaceted approach. Cost control is paramount; businesses must continuously strive to optimize expenses without compromising quality or service. This might involve negotiating better deals with suppliers, streamlining operational processes, or investing in technology to improve efficiency. Simultaneously, increasing revenue is crucial. Strategies include expanding into new markets, developing innovative products or services, or implementing effective marketing campaigns to boost sales.

Regularly monitoring key performance indicators (KPIs) and making data-driven adjustments are also essential for sustaining profitability. For example, a restaurant might analyze customer feedback to identify popular dishes and adjust their menu accordingly, while simultaneously exploring options to reduce food waste.

Using Net Profit Margin Data for Investment Decisions

Investors use net profit margin data to assess the financial health and potential return on investment of a company. A consistently high net profit margin suggests a company’s ability to generate strong profits, making it an attractive investment prospect. Conversely, a low or declining net profit margin might raise concerns about the company’s long-term viability and potential for future returns.

For example, an investor comparing two companies in the same industry would likely favor the company with the higher net profit margin, assuming all other factors are relatively equal. This metric, when considered alongside other financial ratios and market analysis, helps investors make informed decisions about where to allocate their capital.

Profit Margins

Understanding profit margins is crucial for assessing a business’s financial health and performance. Different types of profit margins offer unique insights into various aspects of profitability, allowing for a more comprehensive analysis than relying on a single metric. This section delves into the nuances of gross, operating, and net profit margins, highlighting their individual strengths and how they can be used collectively to gain a clearer picture of a company’s efficiency and overall success.

Types of Profit Margins

Profit margins are calculated by dividing profit by revenue, but the type of profit used determines the specific insight gained. Gross profit margin focuses on the direct costs of production, operating profit margin considers both direct and indirect costs related to operations, and net profit margin encompasses all expenses, including taxes and interest. Each provides a different perspective on profitability.

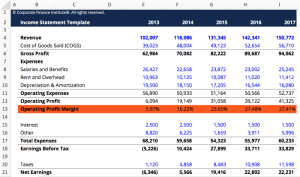

- Gross Profit Margin: This measures the profitability of a company’s core operations after accounting for the direct costs of producing goods or services. It’s calculated as (Revenue – Cost of Goods Sold) / Revenue. A high gross profit margin suggests efficient production and strong pricing power.

- Operating Profit Margin: This reflects profitability after considering both direct and indirect operating expenses, such as salaries, rent, and utilities. It’s calculated as (Revenue – Cost of Goods Sold – Operating Expenses) / Revenue. A strong operating profit margin indicates effective management of operational costs.

- Net Profit Margin: This represents the ultimate profitability after all expenses, including taxes and interest, are deducted. It’s calculated as (Net Income) / Revenue. It provides the clearest picture of a company’s overall profitability and its ability to generate returns for its investors.

Comparing and Contrasting Profit Margin Usefulness

While all three profit margins are valuable, their applications differ depending on the analytical goal. Gross profit margin is useful for assessing the efficiency of production and pricing strategies. Operating profit margin provides a broader view of operational efficiency, encompassing both direct and indirect costs. Net profit margin offers the most comprehensive picture of overall profitability, taking into account all expenses and reflecting the bottom line.

Analyzing these margins together provides a more holistic understanding of a company’s financial performance. For example, a company might have a high gross profit margin but a low operating profit margin, suggesting high operating expenses that need attention.

Using Profit Margin Data to Assess Segment Efficiency

Profit margin analysis can be extended to individual business segments to pinpoint areas of strength and weakness. By calculating the different profit margins for each segment, a company can identify which segments are most profitable and which require improvement. This allows for strategic resource allocation and informed decision-making. For instance, a retail company might find that its online segment has a higher net profit margin than its brick-and-mortar stores, suggesting a shift in investment might be beneficial.

Illustrative Flowchart of Revenue, Costs, and Profit Margins

The relationship between revenue, costs, and the various profit margins can be visualized using a flowchart.[Diagram Description: The flowchart begins with “Revenue” at the top. A downward arrow leads to a branching point labeled “Costs.” One branch goes to “Cost of Goods Sold (COGS),” leading to “Gross Profit.” Another branch from “Costs” goes to “Operating Expenses,” which leads to “Operating Profit.” From “Operating Profit,” another downward arrow leads to “Other Expenses (e.g., Interest, Taxes),” finally resulting in “Net Profit.” Each profit level is linked to its corresponding margin calculation: Gross Profit Margin = (Revenue – COGS)/Revenue; Operating Profit Margin = (Revenue – COGS – Operating Expenses)/Revenue; Net Profit Margin = Net Profit/Revenue.

Arrows clearly indicate the sequential deduction of costs and the resulting profit levels.]

Impact of Cost Management on Net Profit Margin

Effective cost management is paramount to achieving a healthy net profit margin. By strategically controlling expenses, businesses can significantly boost their profitability and enhance their overall financial health. This involves a multifaceted approach that encompasses various aspects of the business operation, from streamlining production processes to optimizing marketing strategies. Ultimately, a reduction in costs directly translates to a higher net profit margin, assuming revenue remains constant or increases.

The relationship between cost management and net profit margin is directly proportional. A decrease in costs, while maintaining or increasing revenue, leads to a higher net profit margin. Conversely, uncontrolled costs can severely erode profitability, even with strong sales figures. Therefore, implementing effective cost-cutting measures is a crucial aspect of long-term business sustainability and growth. This involves a detailed analysis of all expenses, identifying areas for potential savings, and then implementing strategies to achieve those savings without compromising the quality of products or services offered.

Cost-Cutting Strategies for Improved Net Profit Margin

Several strategies can be implemented to effectively cut costs and improve the net profit margin. These strategies range from streamlining internal processes to negotiating better deals with suppliers. Careful planning and execution are essential to ensure that cost-cutting measures do not negatively impact product quality or customer satisfaction.

One effective approach is to analyze the cost of goods sold (COGS). Identifying areas within the production process where efficiencies can be gained can lead to significant savings. This might involve investing in new technology, streamlining workflows, or negotiating better terms with suppliers. Another crucial area to focus on is operational expenses, which include rent, utilities, and salaries.

Reviewing contracts with vendors and exploring alternative options can often lead to substantial savings. Marketing and advertising costs can also be optimized by focusing on more efficient and targeted campaigns, leveraging digital marketing strategies and analyzing the return on investment (ROI) for each campaign.

Case Studies of Successful Cost Control

Many companies have demonstrated the power of cost control in boosting their net profit margins. For example, Walmart, known for its efficient supply chain and low-cost strategy, consistently maintains a high net profit margin by focusing on cost optimization across its entire operation. Their sophisticated logistics and inventory management systems minimize waste and maximize efficiency. Similarly, McDonald’s, through its standardized processes and economies of scale, maintains tight control over its costs, contributing to a healthy profit margin.

Their focus on efficiency in food preparation and streamlined operations allows them to offer competitively priced menu items while maintaining profitability. These companies showcase the potential for substantial improvements in net profit margins through diligent cost management.

Strategies for Managing Costs to Improve Profit Margins

A well-defined cost management strategy requires a multi-pronged approach. It’s not simply about cutting costs; it’s about optimizing expenses while maintaining quality and service levels. A holistic approach is necessary to achieve lasting improvements.

- Negotiate better terms with suppliers: Explore opportunities to negotiate lower prices or improved payment terms with suppliers. This can significantly impact the cost of goods sold.

- Improve operational efficiency: Streamline processes, eliminate redundancies, and invest in technology to automate tasks and improve productivity. This can reduce labor costs and improve overall efficiency.

- Optimize inventory management: Implement strategies to minimize inventory holding costs, reduce waste, and improve inventory turnover. This minimizes storage costs and prevents losses from obsolete inventory.

- Reduce energy consumption: Implement energy-saving measures, such as switching to LED lighting or upgrading equipment, to reduce utility costs.

- Implement a robust budgeting and forecasting system: This allows for proactive cost management and helps identify potential cost overruns early on.

- Regularly review and analyze expenses: Conduct regular reviews of expenses to identify areas for potential savings and track the effectiveness of cost-cutting measures.

Net Profit Margin and Pricing Strategies

Pricing strategies are fundamentally linked to a company’s net profit margin. The prices set for products or services directly influence revenue, and subsequently, the ultimate profit realized after deducting all costs. A well-defined pricing strategy, informed by market analysis and cost considerations, is crucial for achieving and maintaining a healthy net profit margin.The relationship between pricing strategies and net profit margin is directly proportional.

Higher prices, all else being equal, lead to a higher net profit margin. However, this relationship is not always simple; pricing too high can deter customers and reduce sales volume, potentially negating the benefit of higher prices per unit. Conversely, pricing too low might increase sales volume but severely compress the profit margin per unit. Finding the optimal balance is key to maximizing profitability.

Value-Based Pricing and its Effect on Net Profit Margin

Value-based pricing focuses on the perceived value a product or service offers to the customer. Instead of solely considering costs, this strategy sets prices based on the benefits customers receive. For example, a luxury car manufacturer might price its vehicles significantly higher than competitors due to the perceived value of superior quality, prestige, and features. This approach can yield a higher net profit margin if the perceived value justifies the higher price point and generates sufficient demand.

However, if customers do not perceive the value, the strategy can backfire, leading to lower sales and potentially a lower net profit margin.

Cost-Plus Pricing and its Effect on Net Profit Margin

Cost-plus pricing is a simpler approach where a fixed percentage markup is added to the cost of production to determine the selling price. This method guarantees a minimum profit margin, but it can be inflexible and less responsive to market dynamics. Imagine a bakery using cost-plus pricing: they calculate their production costs per loaf of bread and then add a 20% markup.

This provides a consistent profit margin on each loaf. However, if competitors offer similar bread at a lower price, the bakery may lose market share despite its consistent profit margin per loaf. The rigidity of this method might limit the potential for maximizing net profit margin.

Optimizing Pricing to Maximize Net Profit Margin

Optimizing pricing requires a multi-faceted approach. It involves careful analysis of cost structures, market demand, competitor pricing, and customer willingness to pay. Companies can use sophisticated pricing models and software to simulate the impact of different price points on revenue and profit. Furthermore, regularly monitoring sales data and customer feedback allows for dynamic price adjustments to maximize profitability.

A key aspect is understanding price elasticity – how sensitive demand is to price changes. Products with inelastic demand (less sensitive to price changes) offer more flexibility in pricing strategies, allowing for potentially higher profit margins.

Utilizing Market Research to Inform Pricing Decisions

Market research plays a critical role in optimizing pricing for maximum net profit margin. Techniques like surveys, focus groups, and competitive analysis provide valuable insights into customer preferences, price sensitivity, and the competitive landscape. By understanding the perceived value of a product or service in relation to its price, businesses can make informed pricing decisions. For example, a company launching a new software application could conduct surveys to gauge customer willingness to pay for different feature sets, allowing them to price the product strategically to maximize profitability while maintaining market competitiveness.

Analyzing competitor pricing strategies also helps determine a competitive yet profitable price point.

In conclusion, mastering the concept of net profit margin empowers businesses to make informed strategic decisions. By diligently analyzing trends, comparing performance against industry benchmarks, and implementing effective cost management and pricing strategies, companies can optimize their profitability and achieve sustainable growth. Understanding net profit margin isn’t just about numbers; it’s about understanding the overall health and potential of your business.

Q&A

What is the difference between gross profit margin and net profit margin?

Gross profit margin considers revenue minus the cost of goods sold, while net profit margin accounts for all expenses, including operating costs, taxes, and interest, providing a more comprehensive picture of profitability.

How can a low net profit margin be improved?

Strategies include reducing operating costs, increasing prices strategically, improving efficiency, and diversifying revenue streams.

Is a high net profit margin always good?

While a high net profit margin is generally desirable, it’s crucial to consider industry benchmarks and the overall financial health of the company. An exceptionally high margin might indicate underinvestment or unsustainable practices.

How frequently should net profit margin be analyzed?

Regular analysis, ideally monthly or quarterly, allows for timely identification of trends and potential issues, enabling proactive adjustments to business strategies.