Understanding and managing profit margins is crucial for any business aiming for sustainable growth. A healthy profit margin isn’t just about maximizing earnings; it’s about ensuring long-term viability, allowing for reinvestment, and navigating economic fluctuations. This guide explores the multifaceted nature of profit margins, delving into calculation methods, influencing factors, and strategies for improvement.

We’ll examine various types of profit margins – gross, operating, and net – and demonstrate how to calculate them using real-world examples. We’ll also investigate both internal factors, such as pricing strategies and operational efficiency, and external factors, including competition and market trends, which significantly impact a company’s profitability. The goal is to equip you with the knowledge to analyze, benchmark, and ultimately improve your profit margins.

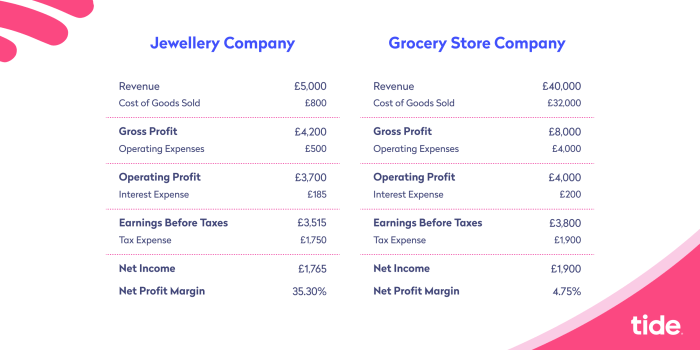

Calculating Profit Margin Percentage

Understanding profit margins is crucial for assessing a business’s financial health and profitability. Different types of profit margins offer varying perspectives on profitability, considering different levels of expenses. This section will detail the calculation and interpretation of three key profit margins: gross profit margin, operating profit margin, and net profit margin.

Gross Profit Margin

Gross profit margin represents the profitability of a company’s core business operations after deducting the direct costs of producing goods or services. It provides a clear picture of how efficiently a company manages its production or service delivery. The formula is straightforward and helps to determine the percentage of revenue remaining after covering the direct costs associated with sales.

Gross Profit Margin = (Revenue – Cost of Goods Sold) / Revenue – 100%

A step-by-step calculation using a sample income statement follows:

Let’s assume a company’s income statement shows Revenue of $1,000,000 and Cost of Goods Sold (COGS) of $600,000.

- Step 1: Calculate Gross Profit: Subtract the Cost of Goods Sold from the Revenue: $1,000,000 – $600,000 = $400,000

- Step 2: Calculate Gross Profit Margin: Divide the Gross Profit by the Revenue and multiply by 100%: ($400,000 / $1,000,000)

– 100% = 40%

This indicates that for every dollar of revenue, 40 cents remain after covering the direct costs of production.

Operating Profit Margin

Operating profit margin reveals a company’s profitability from its core operations after accounting for both direct and indirect costs, excluding interest and taxes. This provides a more comprehensive view of operational efficiency than the gross profit margin. It’s a crucial indicator of a company’s ability to manage its expenses effectively and generate profit from its primary activities.

Operating Profit Margin = (Operating Income) / Revenue – 100%

Using the same example, let’s add Operating Expenses of $200,000. Operating Income is calculated as Gross Profit minus Operating Expenses.

- Step 1: Calculate Operating Income: $400,000 (Gross Profit)

-$200,000 (Operating Expenses) = $200,000 - Step 2: Calculate Operating Profit Margin: ($200,000 / $1,000,000)

– 100% = 20%

This shows that 20 cents of every dollar of revenue remain after covering both direct and indirect operational costs.

Net Profit Margin

Net profit margin is the ultimate measure of profitability, reflecting the percentage of revenue remaining after all expenses, including interest and taxes, have been deducted. It provides the clearest picture of a company’s overall financial performance and its ability to generate profit after all costs are considered.

Net Profit Margin = (Net Income) / Revenue – 100%

Extending the example, let’s assume Interest Expense of $20,000 and Income Taxes of $40,000. Net Income is Operating Income minus Interest and Taxes.

- Step 1: Calculate Net Income: $200,000 (Operating Income)

-$20,000 (Interest Expense)

-$40,000 (Income Taxes) = $140,000 - Step 2: Calculate Net Profit Margin: ($140,000 / $1,000,000)

– 100% = 14%

This shows that 14 cents of every dollar of revenue represents the company’s ultimate profit after all expenses.

Analyzing Profit Margins

Understanding profit margins is crucial for business success. A healthy profit margin indicates efficient operations and strong pricing strategies, while a low margin may signal areas needing improvement. Analyzing internal factors offers valuable insights into how to optimize profitability.

Internal Factors Impacting Profit Margins

Several key internal factors significantly influence a company’s profit margins. These factors are interconnected and require a holistic approach to management. Pricing strategies, cost management, and operational efficiency are particularly important. Effective management of these elements allows businesses to control their revenue streams and expenses, ultimately impacting their bottom line.

Pricing Strategies and Their Effects on Profit Margins

Different pricing strategies yield varying impacts on profit margins. Value-based pricing, which sets prices based on perceived customer value, often results in higher margins compared to cost-plus pricing, which adds a fixed markup to the cost of goods. Value-based pricing allows businesses to capture a larger share of the customer’s willingness to pay, thereby increasing profit. Conversely, cost-plus pricing, while simpler to implement, can lead to lower margins if the market is price-sensitive or if competitors offer similar products at lower prices.

A company selling premium, high-demand software might use value-based pricing successfully, while a manufacturer of standardized components might rely more on cost-plus pricing to remain competitive.

Impact of Operational Efficiency on Profit Margins

Improved operational efficiency directly translates to higher profit margins. Streamlining processes, reducing waste, and optimizing resource allocation all contribute to lower costs and increased profitability. The following hypothetical scenario illustrates this:

| Scenario | Revenue | Cost of Goods Sold | Operating Expenses | Profit Margin (%) |

|---|---|---|---|---|

| Before Improvement | $1,000,000 | $600,000 | $250,000 | 15% |

| After Improvement | $1,000,000 | $500,000 | $200,000 | 30% |

In this example, maintaining the same revenue, improvements in operational efficiency (reducing cost of goods sold by $100,000 and operating expenses by $50,000) resulted in a significant increase in profit margin from 15% to 30%. This demonstrates the substantial impact that even modest efficiency gains can have on a company’s profitability. Such improvements could be achieved through initiatives like implementing lean manufacturing techniques, investing in automation, or improving supply chain management.

Analyzing Profit Margins

Understanding profit margins is crucial for business success, but a complete analysis requires considering factors beyond internal operations. External forces significantly impact a company’s ability to maintain or improve its profit margins. These external pressures can be unpredictable and require proactive strategies to mitigate their effects.

External Factors Influencing Profit Margins

Market dynamics, competitive pressures, and macroeconomic trends all exert considerable influence on a company’s profit margins. A strong understanding of these factors is essential for effective financial planning and strategic decision-making. Ignoring these external forces can lead to inaccurate forecasting and ultimately, diminished profitability.

Competition’s Impact on Profitability

Intense competition often forces businesses to reduce prices to remain competitive, directly impacting profit margins. For example, the rise of budget airlines significantly impacted the profit margins of traditional airlines, forcing them to adapt their pricing strategies and streamline operations. Conversely, a lack of competition can allow a business to maintain higher profit margins, but this can also lead to complacency and a lack of innovation.

A healthy balance between competition and market share is ideal for sustainable profitability.

Market Demand and its Influence

Fluctuations in market demand directly affect pricing power and, consequently, profit margins. High demand allows businesses to increase prices, leading to higher profit margins, while low demand often necessitates price reductions to stimulate sales, thereby squeezing margins. Consider the seasonal nature of many products; Christmas decorations, for instance, have high demand and higher margins during the holiday season but much lower demand (and margins) in the off-season.

Effective forecasting of market demand is crucial for adjusting pricing and inventory levels to optimize profitability.

Economic Trends and Raw Material Costs

Economic downturns often lead to reduced consumer spending, forcing businesses to lower prices to maintain sales volume, negatively impacting profit margins. Conversely, periods of economic growth can increase demand and allow for price increases, boosting profitability. Furthermore, changes in raw material costs, such as oil prices or the cost of lumber, directly affect production costs and, therefore, profit margins.

A sudden spike in oil prices, for instance, would increase transportation costs for many businesses, leading to a reduction in profit margins unless prices are adjusted accordingly. Similarly, increased energy prices directly impact manufacturing and operational costs.

Adapting Pricing Strategies to Mitigate External Factors

Responding effectively to external factors often involves adjusting pricing strategies. This might include implementing dynamic pricing models that adjust prices based on real-time market demand and competitor pricing. Another approach involves diversifying product offerings to reduce reliance on single products vulnerable to market fluctuations. Cost-cutting measures, such as streamlining operations or negotiating better terms with suppliers, can also help to protect profit margins.

Furthermore, investing in research and development to create innovative products or services can provide a competitive edge and allow for premium pricing. The key is flexibility and responsiveness to changing market conditions.

Ultimately, achieving and maintaining a healthy profit margin is a dynamic process requiring continuous monitoring, adaptation, and strategic decision-making. By understanding the intricacies of profit margin calculation, identifying key influencing factors, and implementing effective improvement strategies, businesses can pave the way for long-term success and sustainability. Regular benchmarking against industry averages and competitors will help maintain a competitive edge and identify areas ripe for optimization.

FAQ Corner

What is a good profit margin percentage?

A “good” profit margin varies significantly across industries. A high-margin industry might consider 20% excellent, while a low-margin industry might be satisfied with 5%. Benchmarking against competitors within your specific industry is key.

How often should I analyze my profit margins?

Regular analysis is crucial. Monthly or quarterly reviews allow for timely adjustments to strategies and identification of potential issues before they become major problems. Annual analysis provides a longer-term perspective on trends.

What are some common mistakes businesses make when managing profit margins?

Common mistakes include underpricing products or services, failing to adequately control costs, neglecting market research, and not adapting to changing economic conditions. Ignoring benchmarking data is another frequent oversight.